In this page we introduce the usage of function gwr_basic().

library(sf)

#> Linking to GEOS 3.7.1, GDAL 2.4.0, PROJ 5.2.0; sf_use_s2() is TRUE

library(GWmodel3)

#>

#> Attaching package: 'GWmodel3'

#> The following object is masked from 'package:stats':

#>

#> stepModel Calibration

We use the LondonHP data as an example to demonstrate how to use function gwr_basic(). Assume that the PURCHASE is the dependent variable, while FLOORSZ and UNEMPLOY are independent varaibles. We can build a GWR model through the folloing way.

data(LondonHP)

m1 <- gwr_basic(

formula = PURCHASE ~ FLOORSZ + UNEMPLOY + PROF,

data = LondonHP,

bw = 64,

adaptive = TRUE

)

m1

#> Geographically Weighted Regression Model

#> ========================================

#> Formula: PURCHASE ~ FLOORSZ + UNEMPLOY + PROF

#> Data: LondonHP

#> Kernel: gaussian

#> Bandwidth: 64 (Nearest Neighbours)

#>

#>

#> Summary of Coefficient Estimates

#> --------------------------------

#> Coefficient Min. 1st Qu. Median 3rd Qu. Max.

#> Intercept -198642.679 -182675.271 -165665.781 -134650.946 -93550.292

#> FLOORSZ 1189.823 1309.140 1399.934 1668.918 1840.670

#> UNEMPLOY 311994.460 531503.077 663356.786 735359.196 932328.652

#> PROF 243840.288 319870.143 355123.025 378312.489 429390.257

#>

#>

#> Diagnostic Information

#> ----------------------

#> RSS: 4.56323e+11

#> ENP: 14.12809

#> EDF: 301.8719

#> R2: 0.7451855

#> R2adj: 0.7332201

#> AIC: 7571.953

#> AICc: 7585.417Compared with GWmodel, the usage is changed in the following ways:

- The function is renamed to

gwr_basicto avoid conflicts with the old version. - The function no longer support the

regression.pointsargument. To predict at new locations, please use thepredict()function. - The OLS part is no longer shown in outputs of the return value. Users can call

lm()function with specified arguments.

This function return a gwrm object. Through the outputs in console, we can get infromation of fomula, data, kernel, bandwidth, coefficient estimates, and diagnostics. Besides, it is supported to get more infromation via coef() fitted() residuals().

head(coef(m1))

#> Intercept FLOORSZ UNEMPLOY PROF

#> 0 -124453.6 1287.804 528674.5 295482.3

#> 1 -122812.0 1282.712 520067.3 293203.2

#> 2 -122487.0 1281.506 530303.5 291236.4

#> 3 -121768.6 1278.788 527744.3 290153.6

#> 4 -122064.9 1278.969 520144.8 291861.3

#> 5 -101753.7 1234.532 396245.5 263582.0

head(fitted(m1))

#> [1] 135011.1 132297.2 117858.7 157436.0 173050.9 157071.0

head(residuals(m1))

#> [1] 21988.936 -18797.233 -36108.677 -7436.005 16949.120 2879.028In addition, like GWmodel, gwrm objects provide a $SDF variable which contains coefficient estimates and other sample-wise results.

head(m1$SDF)

#> Simple feature collection with 6 features and 14 fields

#> Geometry type: POINT

#> Dimension: XY

#> Bounding box: xmin: 531900 ymin: 159400 xmax: 535700 ymax: 161700

#> CRS: NA

#> Intercept FLOORSZ UNEMPLOY PROF yhat residual Intercept.SE

#> 0 -124453.6 1287.804 528674.5 295482.3 135011.1 21988.936 5839925

#> 1 -122812.0 1282.712 520067.3 293203.2 132297.2 -18797.233 5873318

#> 2 -122487.0 1281.506 530303.5 291236.4 117858.7 -36108.677 5962947

#> 3 -121768.6 1278.788 527744.3 290153.6 157436.0 -7436.005 5990687

#> 4 -122064.9 1278.969 520144.8 291861.3 173050.9 16949.120 5928749

#> 5 -101753.7 1234.532 396245.5 263582.0 157071.0 2879.028 6126740

#> FLOORSZ.SE UNEMPLOY.SE PROF.SE Intercept.TV FLOORSZ.TV UNEMPLOY.TV

#> 0 351842.1 14680113 7170057 -0.02131082 0.003660175 0.03601297

#> 1 353135.2 14735103 7214234 -0.02091015 0.003632355 0.03529444

#> 2 356231.7 14939953 7324666 -0.02054135 0.003597394 0.03549566

#> 3 357162.0 14994222 7360524 -0.02032632 0.003580416 0.03519651

#> 4 354868.2 14840291 7285505 -0.02058864 0.003604066 0.03504950

#> 5 363613.1 15108910 7586125 -0.01660813 0.003395180 0.02622595

#> PROF.TV geometry

#> 0 0.04121060 POINT (533200 159400)

#> 1 0.04064233 POINT (533300 159700)

#> 2 0.03976104 POINT (532000 159800)

#> 3 0.03942024 POINT (531900 160100)

#> 4 0.04006054 POINT (532800 160300)

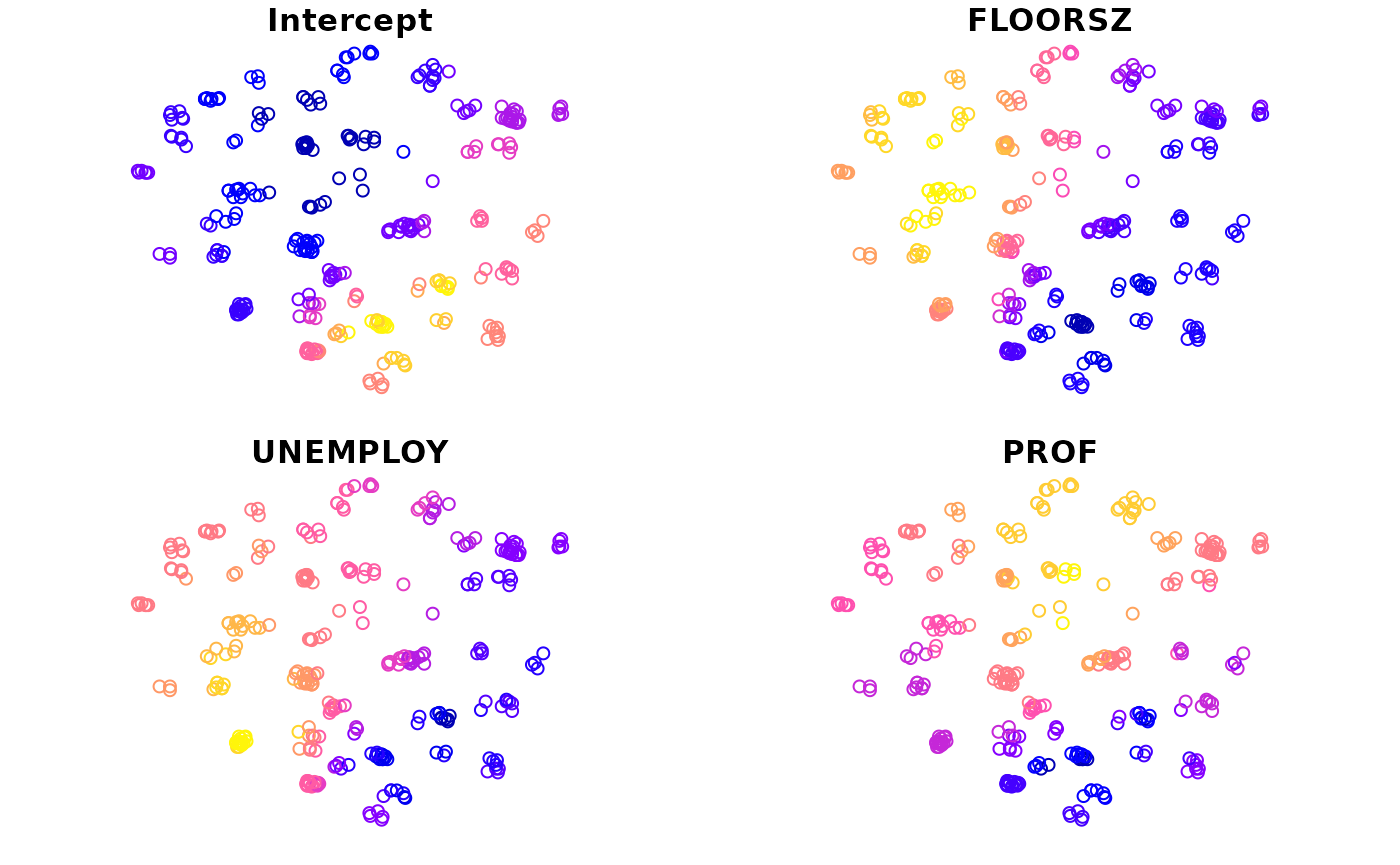

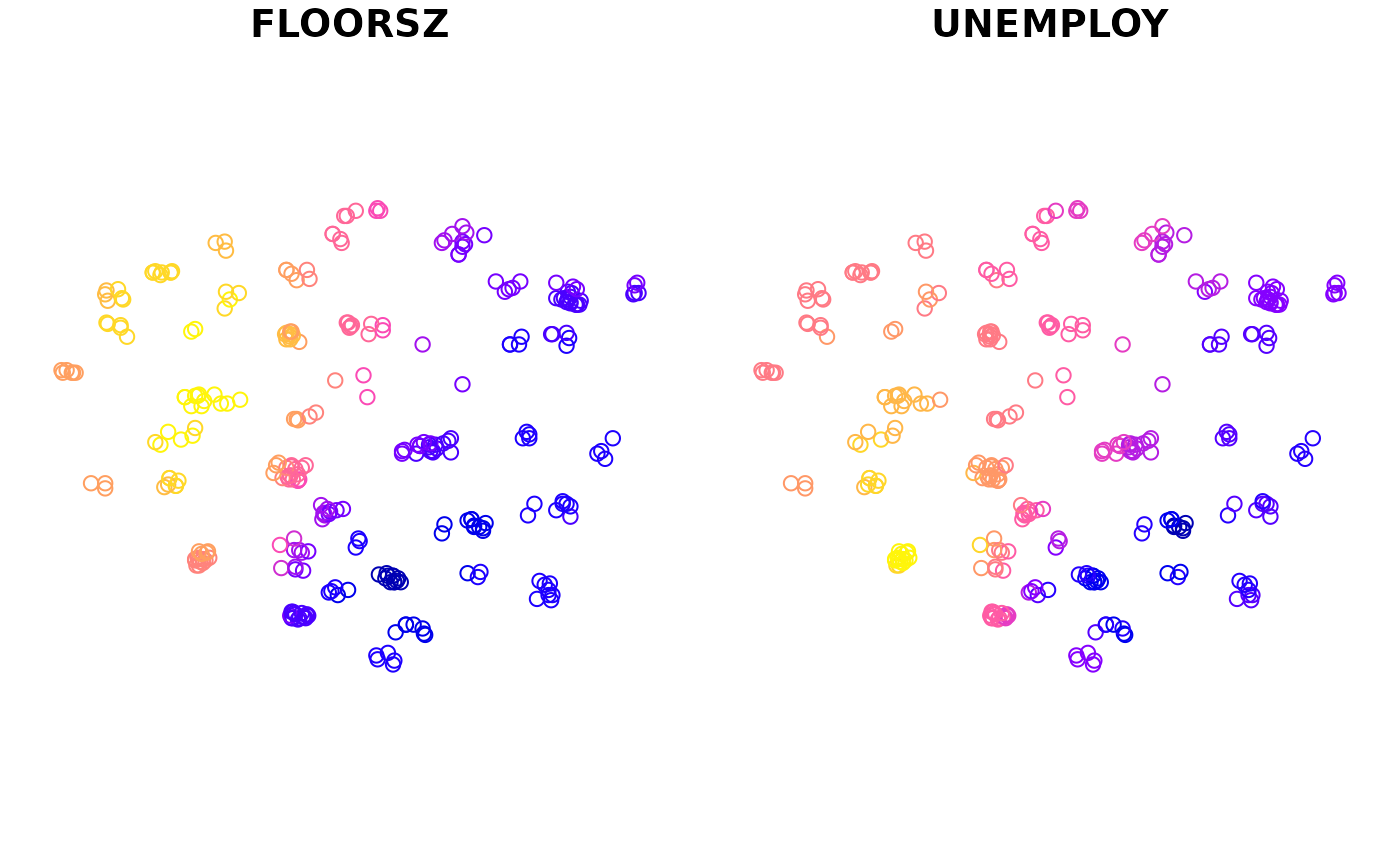

#> 5 0.03474527 POINT (535700 161700)We can create maps with this variable. There is a plot() function provided to preview coefficient estimates easily.

plot(m1)

If the second argument is omitted, all coefficient estimates will be mapped by default. Otherwise, only specified variables will be mapped.

Bandwidth Optimization

We can call the function in the following way when we want the function to get an optimized bandwidth instead.

data(LondonHP)

m <- gwr_basic(

formula = PURCHASE ~ FLOORSZ + UNEMPLOY,

data = LondonHP,

bw = "AIC",

adaptive = TRUE

)

message("Bandwidth:", m$args$bw)

#> Bandwidth:20The method for optimizing bandwidth is specified through strings "AIC" or "CV". Besides, when argument bw is missing or set to non-numeric values, this function select an optimized bandwidth according to AIC values.

To obtain the value of optimized bandwidth, use the variable $args$bw of the returned object, or read it from console output.

Model Selection

In this package, there is a generic function called step(). We we apply it to gwrm objects, it can select variables, just like the stepAIC() in MASS.

m2 <- gwr_basic(

PURCHASE ~ FLOORSZ + UNEMPLOY + PROF + BATH2 + BEDS2 + GARAGE1 +

TYPEDETCH + TPSEMIDTCH + TYPETRRD + TYPEBNGLW + BLDPWW1 +

BLDPOSTW + BLD60S + BLD70S + BLD80S + CENTHEAT,

LondonHP, "AIC", TRUE

)

m2 <- step(m2, criterion = "AIC", threshold = 10, bw = Inf, optim_bw = "AIC")

m2

#> Geographically Weighted Regression Model

#> ========================================

#> Formula: PURCHASE ~ FLOORSZ + PROF + UNEMPLOY

#> Data: LondonHP

#> Kernel: gaussian

#> Bandwidth: 20 (Nearest Neighbours) (Optimized accroding to AIC)

#>

#>

#> Summary of Coefficient Estimates

#> --------------------------------

#> Coefficient Min. 1st Qu. Median 3rd Qu. Max.

#> Intercept -283403.492 -202450.678 -146322.221 -26250.365 75680.532

#> FLOORSZ 908.249 1095.711 1411.257 1864.155 2482.376

#> PROF -16595.354 143221.798 303155.382 379563.029 480351.828

#> UNEMPLOY -982984.259 -5935.799 575766.002 1029212.413 1780751.157

#>

#>

#> Diagnostic Information

#> ----------------------

#> RSS: 348701748965

#> ENP: 40.26956

#> EDF: 275.7304

#> R2: 0.8052821

#> R2adj: 0.7767406

#> AIC: 7506.818

#> AICc: 7546.36There are two arguments: bw and optim_bw. This is the way to use them:

- When

bwis missing or isNA, then the bandwidth recorded ingwrmobject is used. - When

bwis numeric, its value is used in model optimization. The value ofoptim_bwdetermined whether optimize bandwidth again before finally calibrate it.- When

optim_bwis"no", skip the bandwidth optimization process. - When

optim_bwis"AIC"or"CV", optimize bandwidth according to the corresponding criterion.

- When

- When

bwis non-numeric, useInfas the bandwidth value to optimize bandwidth. And use the criterion specified byoptim_bwto optimize bandwidth. Whenoptim_bwis"no", use the AIC criterion by default.

It seems to be complicated, but it is easy to use. On most occassions, set paramters like the example above.

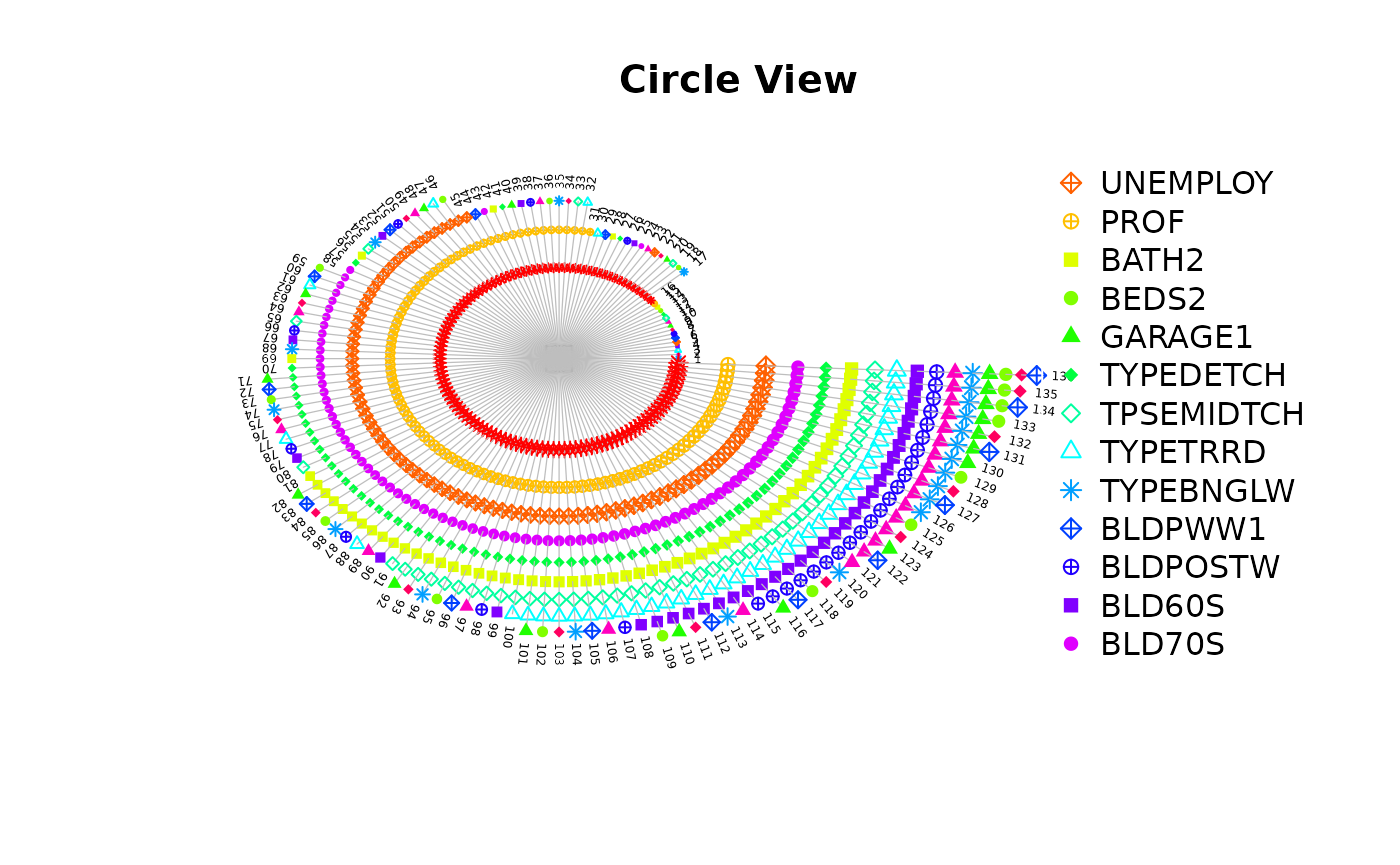

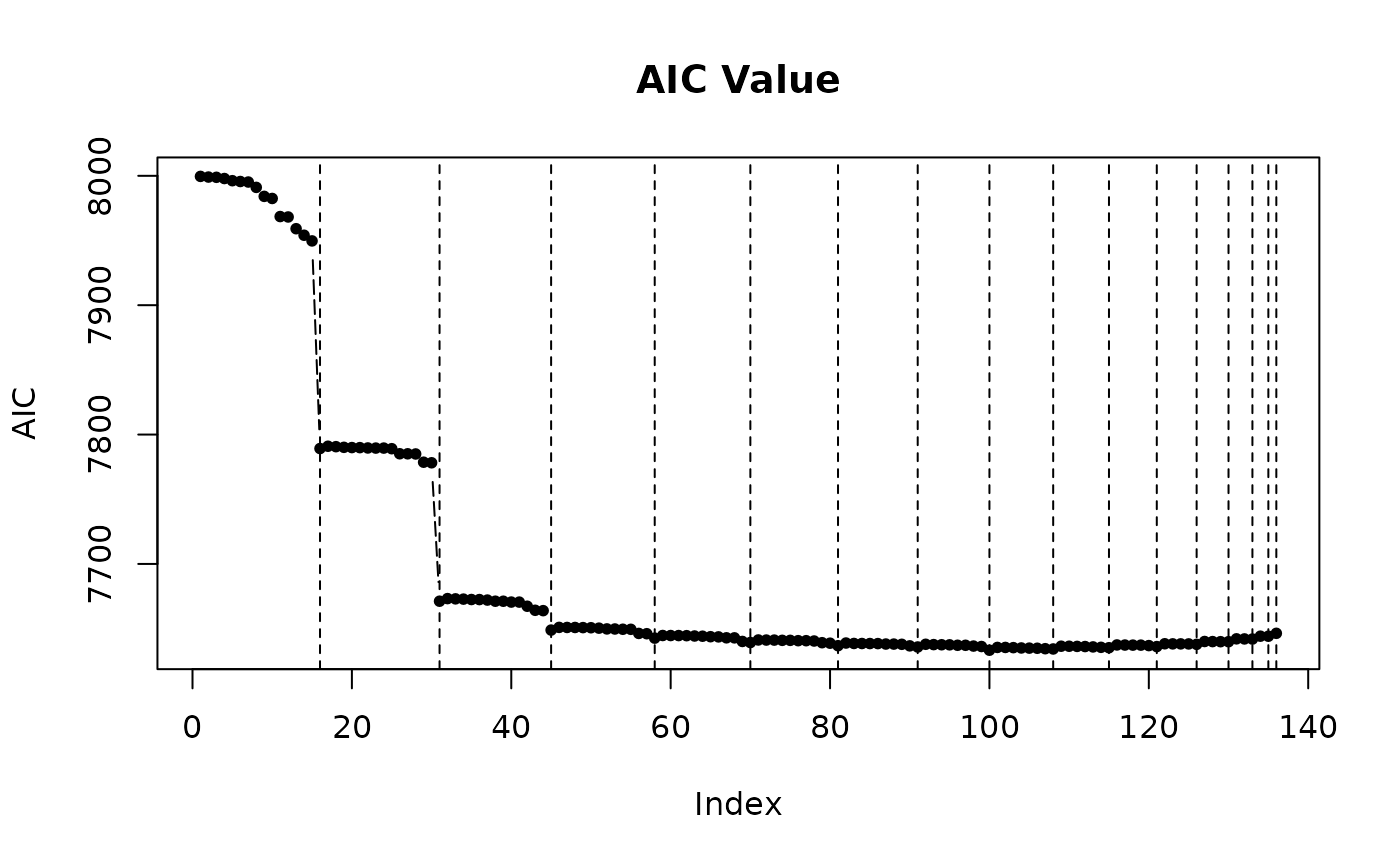

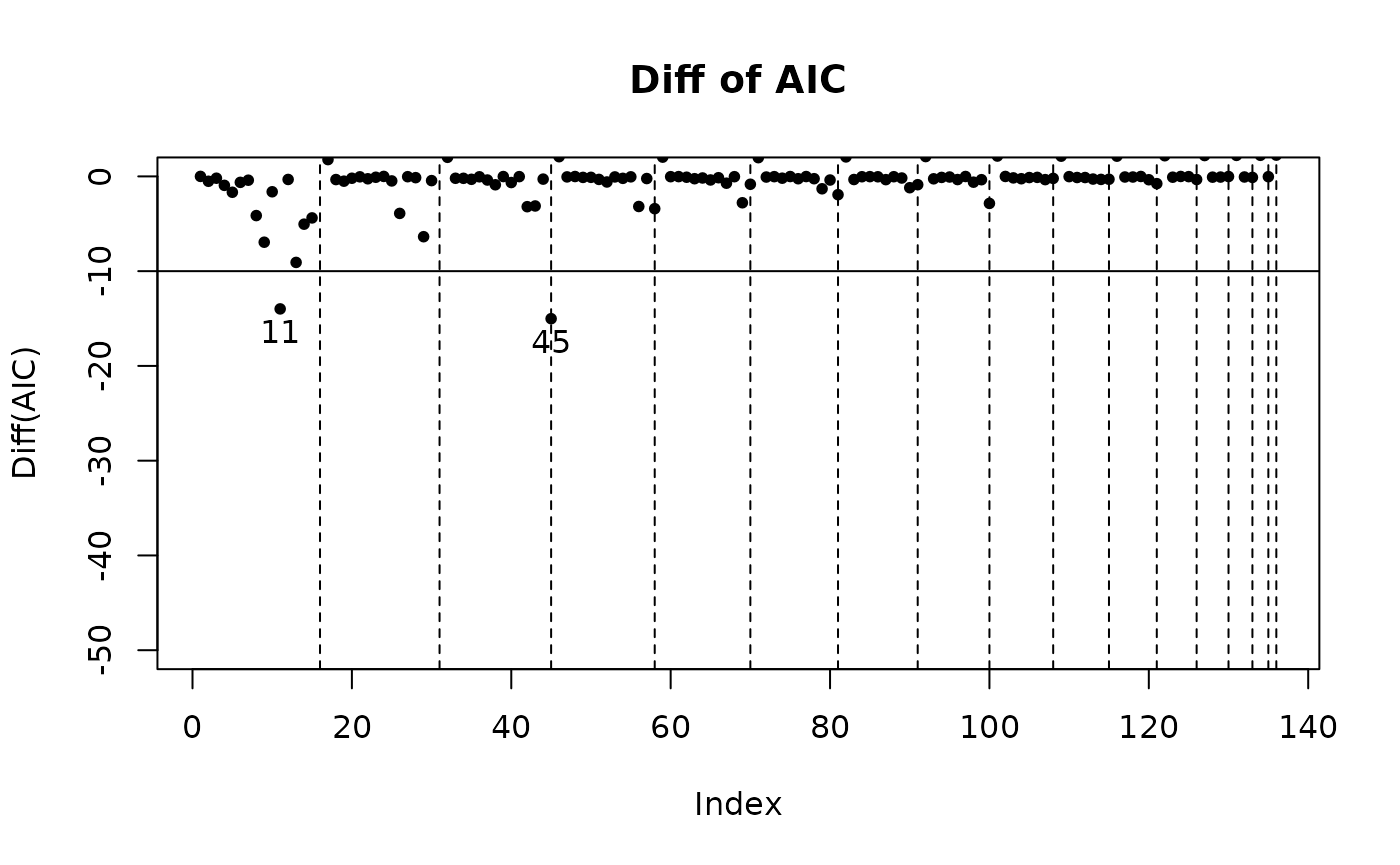

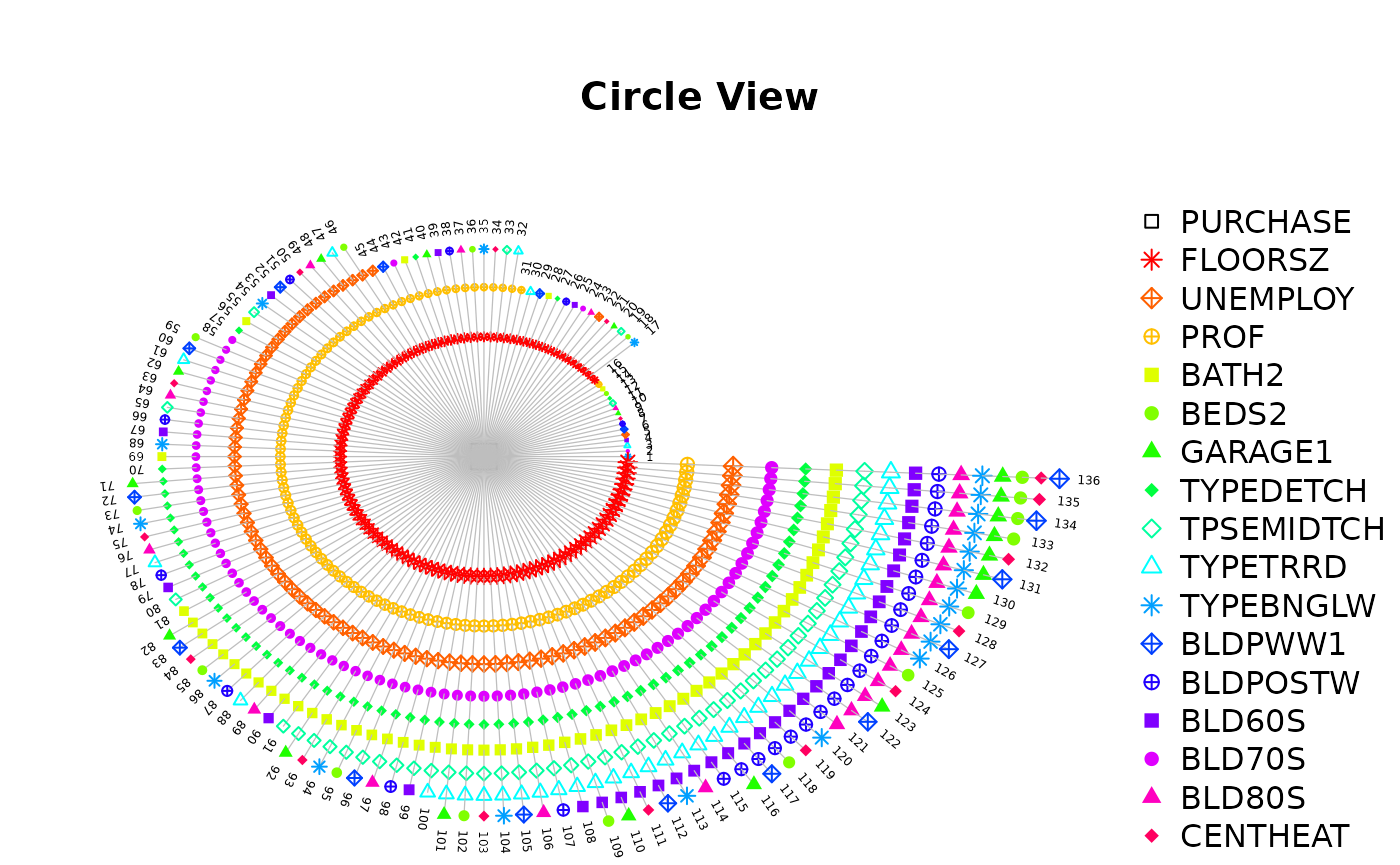

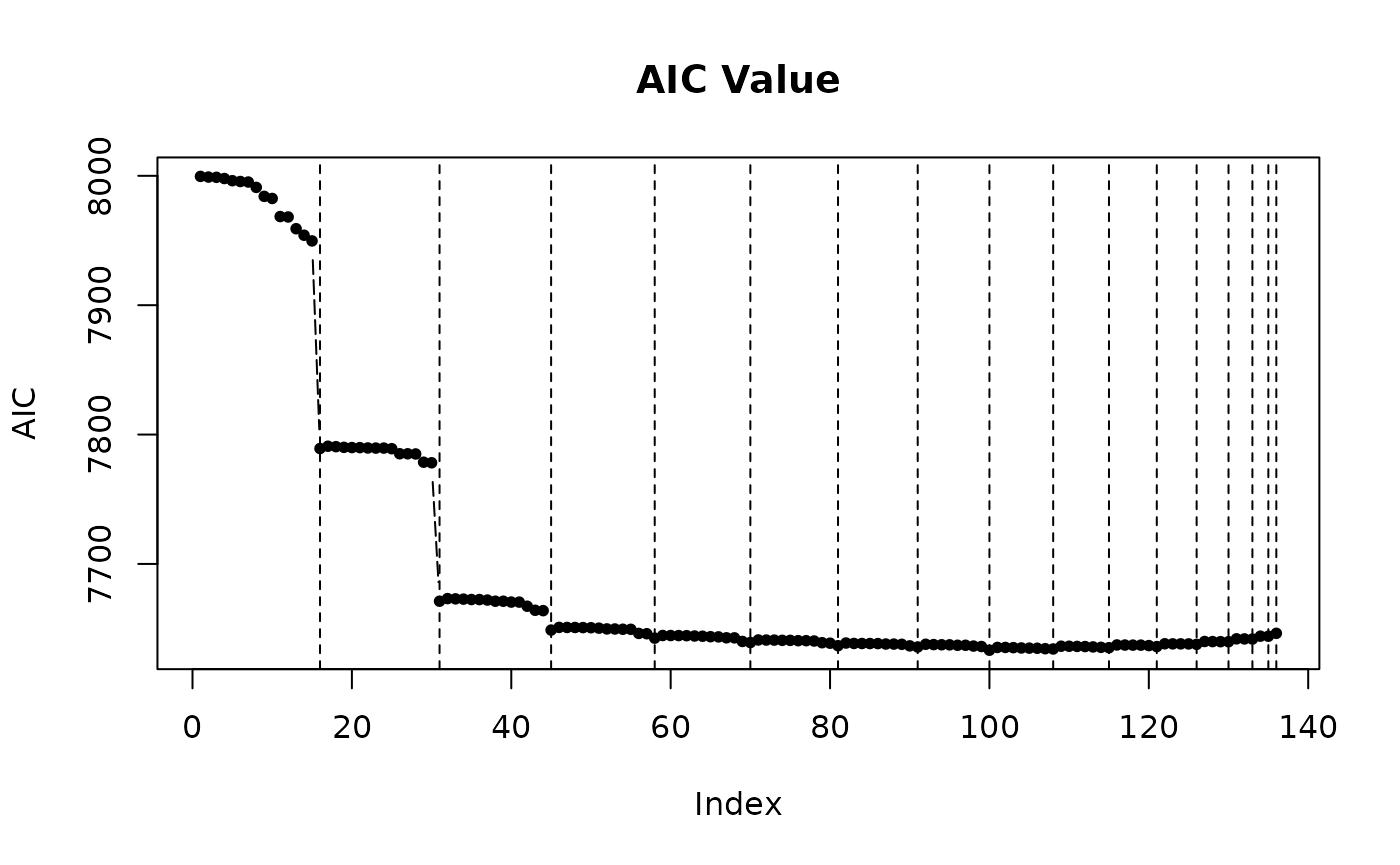

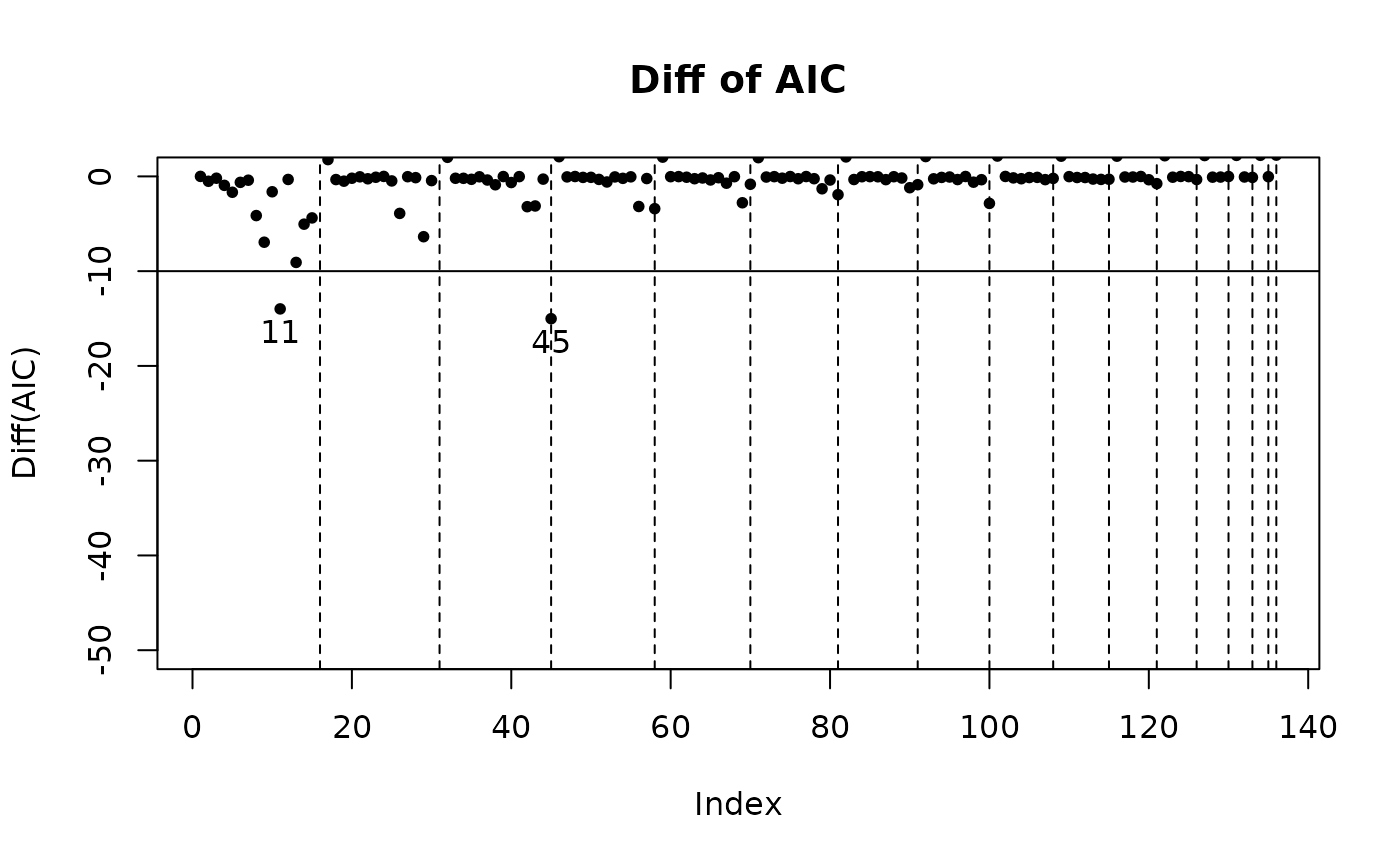

The returned object after model selection contains a $step variable, in which there are all model combinations and corresponding criterions. There are three functions to visualize it.

step_view_circle(m2$step, main = "Circle View")

step_view_value(m2$step, main = "AIC Value")

step_view_diff(m2$step, main = "Diff of AIC")

We can also use the universal plot() function which will make some modification to layouts.

plot(m2$step, main = "Circle View") # step_view_circle

plot(m2$step, main = "AIC Value", view = "value") # step_view_value

plot(m2$step, main = "Diff of AIC", view = "diff") # step_view_diff

If further modification is required, use other arguments supported by plot().

Predict

Based on the current model, GWR can predict coefficient values at any position. We can use predict() function.

predict(m2, LondonHP)

#> Simple feature collection with 316 features and 6 fields

#> Geometry type: POINT

#> Dimension: XY

#> Bounding box: xmin: 507400 ymin: 159400 xmax: 552300 ymax: 194900

#> CRS: NA

#> First 10 features:

#> Intercept FLOORSZ PROF UNEMPLOY yhat residual

#> 0 -23859.461 1107.8783 143091.28 -68568.68 127499.2 29500.837

#> 1 -19273.643 1099.6911 137317.02 -105774.02 125164.0 -11664.024

#> 2 -22341.033 1101.6762 139576.72 -78733.42 112173.3 -30423.269

#> 3 -16587.207 1091.7319 131959.65 -127715.69 145741.0 4259.021

#> 4 -4548.212 1071.6907 118805.43 -236130.77 158572.5 31427.480

#> 5 36721.681 1025.9964 69162.51 -574801.77 158491.4 1458.602

#> 6 41385.027 1015.8069 64587.38 -621772.02 139520.0 10475.019

#> 7 41586.375 980.2804 72971.83 -702105.05 206972.8 32977.160

#> 8 57682.066 985.6583 47493.74 -778290.44 158200.9 -5200.854

#> 9 71221.072 928.7546 43974.22 -982984.26 310010.7 -60060.651

#> geometry

#> 0 POINT (533200 159400)

#> 1 POINT (533300 159700)

#> 2 POINT (532000 159800)

#> 3 POINT (531900 160100)

#> 4 POINT (532800 160300)

#> 5 POINT (535700 161700)

#> 6 POINT (535600 161800)

#> 7 POINT (533400 161900)

#> 8 POINT (535500 162200)

#> 9 POINT (534200 162500)The result varies depends on the second argument:

- When it is a

sforsfcobject, the function will return asforsfcobject including the orignal geometries. - When it is a two-column matrix or

data.frame, the function will return adata.frameobject without geometries.

Besides, when the second argument is a sf or sfc object, the returned value varies depends on its attributes:

- When it does not contains all of independent variables, only coefficient estimates will be returned.

- When it only contains all of independent variables, coefficient and dependent variable estimates will be returned.

- When it contains all of independent variables and the dependent variable, coefficient estimates, dependent variable estimates and residuals will be returned.

Then we can get different results for different demands.